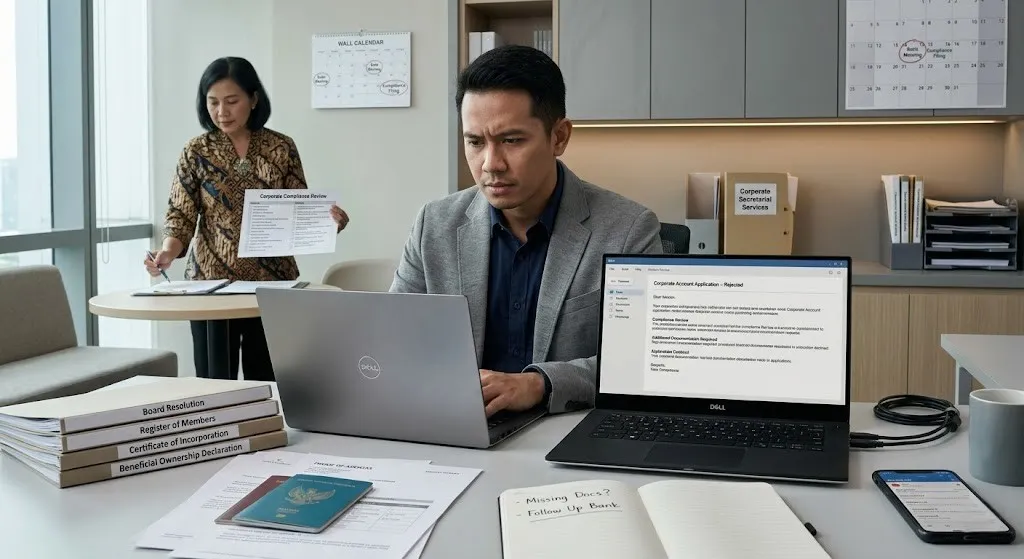

Establishing a new commercial venture frequently feels like navigating an intricate labyrinth before achieving that inaugural sale. Among the most formidable obstacles entrepreneurs encounter is opening a corporate bank account. You complete the necessary documentation, submit supporting materials, and then… absolute silence. Weeks disappear. Your inquiries meet no response. Eventually, a rejection notice arrives.

The frustration proves considerable. Yet understanding the underlying rationale remains paramount. Financial institutions shoulder significant liability when welcoming inappropriate clients. When your application faces denial, personal animosity rarely plays a role. More commonly, compliance deficiencies, incomplete information, or perceived structural vulnerabilities drive the decision.

Countless founders find themselves ensnared within this repetitive cycle. They persistently reapply, only to confront identical outcomes. The fundamental issue typically resides in application preparation methodology. This is precisely where specialized guidance becomes transformative. A seasoned company secretary grasps the specific regulatory criteria banks prioritize. Robust corporate secretarial services ensure your documentation withstands rigorous examination immediately.

The Bank’s Perspective: Risk Management First

Deciphering rejection patterns requires examining the institution’s core mission. Their primary obligation centers upon institutional safeguarding and legal conformity—not entrepreneurial convenience. Every nation enforces stringent financial regulations targeting money laundering prevention, fraud detection, and terrorism financing disruption.

During application review, compliance personnel must authenticate every facet. They require definitive identification of beneficial ownership, capital origins, and authorized fund administrators. Ambiguity surrounding any component generates automatic refusal. Institutions prefer forfeiting potential revenue over absorbing regulatory penalties potentially reaching millions. Regulators conduct random audits assessing whether banks identified questionable transactions. Institutions failing to detect problematic clients face severe sanctions. Consequently, their natural inclination leans toward extreme caution.

You might perceive your submission as comprehensive while reviewers identify gaps. The discrepancy usually stems from granular details. Minor identification document errors, absent signatures on director resolutions, or imprecise business activity descriptions activate warning systems. For entrepreneurs juggling operational demands, mastering these technical nuances proves overwhelming. Engaging a company secretary typically demonstrates prudence. These professionals communicate fluently within regulatory frameworks.

Common Reasons for Account Rejection

Specific problems generate denials more frequently than others. Recognizing these patterns enables effective prevention.

Initially, beneficial ownership transparency creates persistent obstacles. This concept refers to identifying the actual individuals exercising ultimate control over corporate entities. Occasionally, business owners utilize nominee arrangements or elaborate offshore configurations. Banking institutions despise such opacity. Failure to explicitly identify ultimate controllers results in immediate rejection. Even legitimate enterprises trigger suspicion through confusing structures.

Additionally, numerous applicants struggle demonstrating alignment between commercial activities and revenue projections. Consider a trading firm claiming software importation activities. When banking representatives request shipping documentation, absence of such records generates anxiety. Institutions demand evidence of operational traction. Without substantiation, they suspect shell company establishment for illicit financial movement.

Furthermore, governance documentation quality significantly impacts decisions. Have annual submissions been filed? Were mandatory director meetings conducted? Disorganized internal records signal management deficiencies to financial reviewers. They fear that neglected internal oversight indicates potential external financial control failures. A qualified company secretary maintains these critical records current and accessible.

Geographic inconsistencies also create frequent complications. Registered business addresses, residential director locations, and transaction billing addresses require logical coherence. Documentation presenting conflicting information compared to identification materials triggers automated alerts. Minor discrepancies accumulate rapidly during comprehensive due diligence examinations.

Finally, certain sectors attract enhanced scrutiny. Cryptocurrency operations, gaming enterprises, adult entertainment, and international consulting organizations encounter stricter verification protocols. Banks deliberately restrict exposure within these categories. Operating within flagged industries places the evidentiary burden entirely upon the applicant.

What Does a Company Secretary Actually Do?

Many entrepreneurs hearing “company secretary” envision minute-taking or governmental form submission. While accurate partially, contemporary responsibilities extend considerably further. Modern practitioners function as governance specialists possessing comprehensive Companies Act expertise.

They serve as intermediaries connecting commercial operations with statutory requirements. They validate that every strategic decision withstands regulatory examination. Early involvement before bank engagement elevates their contribution from administrative assistance to strategic compliance partnership.

These professionals command regulatory terminology fluently. They distinguish valid identification formats from acceptable corporate resolutions. Beyond simply distributing forms, they examine complete organizational record ecosystems. This encompasses constitutional documents, shareholder registries, and director particulars.

Absent such specialized knowledge, entrepreneurs frequently overlook critical filing deficiencies invisible to untrained eyes. You believe requirements satisfied; banking reviewers perceive otherwise.

How Corporate Secretarial Services Prepare You

Incorporating professional corporate secretarial Singapore during establishment phases fundamentally alters outcomes. Here’s their specific contribution toward banking relationship establishment.

Prior to bank contact, they conduct internal compliance assessments. They examine statutory registers. They confirm proper share capital issuance. They verify current, valid identification for all directors and beneficial owners. This process captures errors before human banking personnel review materials.

Subsequently, they prepare precise documentation matching bank requirements. Institutions request director resolutions authorizing account establishment. These documents require specific phrasing conventions. Self-drafted versions risk omitting essential clauses. Informal presentation risks rejection. Professional secretaries generate correct documentation initially.

They additionally compile supporting evidence systematically. Do invoices exist? Contracts? Address verification? The secretary assembles these into organized portfolios. Clear labeling ensures immediate comprehension. When compliance officers access folders, they encounter transparency. Transparency minimizes processing friction.

Occasionally, they directly communicate with banking representatives regarding your application. They address inquiries arising during investigation phases. Their regulatory requirement comprehension enables precise responses clearing outstanding queries. This capability accelerates processing timelines substantially.

Consider temporal implications. Banking processes require weeks or months. Incomplete applications extend duration significantly through repeated query cycles. Addressing foundational elements beforehand reduces total waiting periods. Earlier operational commencement follows naturally.

The Value of Professional Guidance

Corporate account establishment shouldn’t resemble speculation. Most jurisdictions follow standardized procedures. However, elevated stakes exist because errors incur financial and temporal costs. Engaging external expertise represents risk mitigation rather than simple service procurement.

Some founders hesitate allocating budgets toward corporate secretarial services. They categorize such expenditure as unnecessary overhead. Yet compared against cash flow interruption from frozen accounts, investment costs appear minimal. Operational effectiveness becomes impossible without payment processing or supplier disbursement capabilities.

A proficient company secretary identifies banking institutions likely approving specific profiles based on industry sector. They recognize which institutions specialize in technology ventures versus traditional retail. They direct you toward compatible institutions matching your commercial model. This strategic guidance eliminates unnecessary rejection cycles.

They maintain current awareness as well. Regulatory landscapes evolve continuously. New guidelines regarding digital assets or foreign investment emerge regularly. Dedicated secretaries monitor these developments ensuring ongoing organizational compliance. This vigilance cultivates lasting financial partner confidence.

Moving Forward

Commercial banking operates under strict regulatory frameworks unlikely to relax significantly. Institutions will persist with cautious approaches until complete confidence exists regarding identity and operations. The objective involves eliminating barriers generating such skepticism.

When facing repeated rejections, cease resubmitting identical documentation. Pause for governance evaluation. Examine ownership disclosure accuracy. Review business description precision. Then engage specialized assistance. A company secretary provides structural integrity and confidence necessary for successful banking interactions.

Accurate initial documentation surpasses ten subsequent corrections. Invest adequate preparation time. Secure funding channels early enabling product development and customer service concentration. With appropriate corporate secretarial services implemented, successful account establishment follows a considerably smoother trajectory.

Comments

No comments yet. Be the first to react!